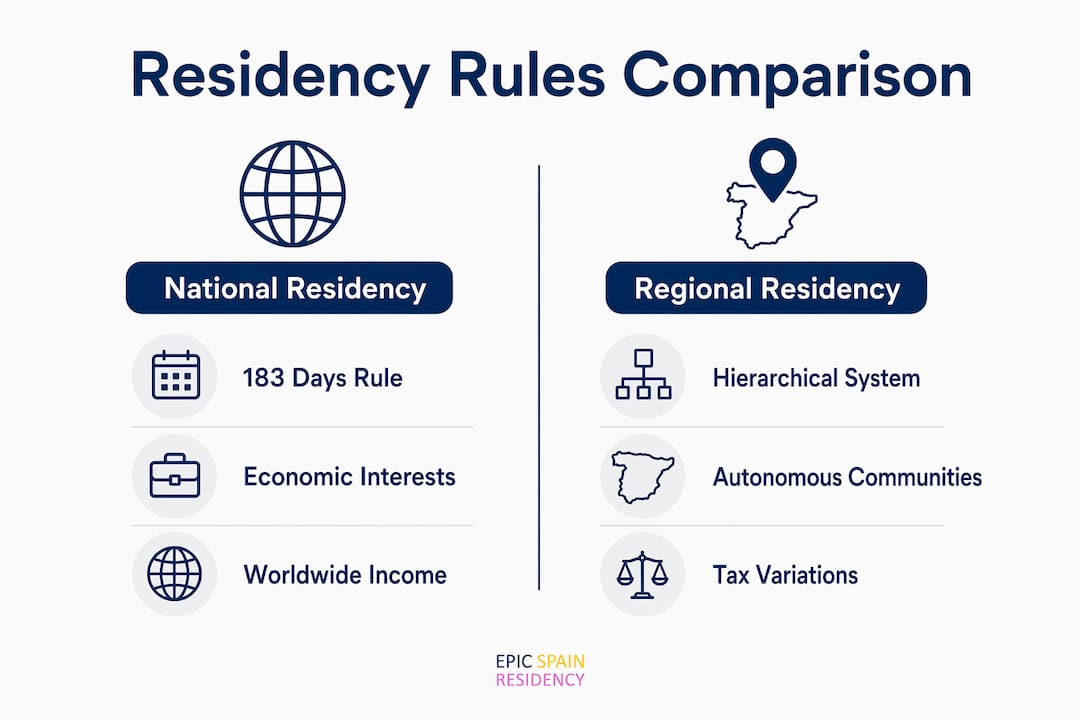

Spanish residency is not a single legal status. It operates on two distinct layers governed by Article 9 LIRPF at the national level and Article 72 LIRPF at the regional level, and confusing the two is one of the most expensive mistakes expats make when moving to Spain. The national layer determines whether you are a Spanish tax resident at all. The regional layer determines which autonomous community claims you, and that distinction directly shapes your wealth tax bill, inheritance tax exposure, and access to social services. Madrid's 100% Net Wealth Tax bonus versus full liability in Catalonia or Valencia is not a minor footnote. For high-net-worth individuals, it can mean tens of thousands of euros per year.

What are Spain's national residency rules under Article 9 LIRPF?

Spain's national tax residency is defined by three inclusive criteria under Article 9 LIRPF: spending 183 or more days in Spain during a calendar year, having your primary center of economic interests in Spain, or having a spouse and dependent children who reside in Spain. Meeting any one of these three criteria is sufficient to qualify as a Spanish tax resident. You do not need to satisfy all three.

The 183-day rule is the most straightforward to track, but the economic interests criterion catches many people off guard. If your main business, investments, or income sources are based in Spain, the Spanish tax authority (Agencia Tributaria) can classify you as a resident even if you spend fewer than 183 days in the country. The family criterion adds another layer: if your spouse and minor children live in Spain, you are presumed to be a resident unless you can prove otherwise.

Once you meet national residency criteria, Spain taxes your worldwide income. This means income from rental properties in the United States, dividends from a UK brokerage, or freelance contracts paid in euros from a German client all fall within Spain's tax reach. Understanding this scope before you move is not optional. It is the foundation of your entire financial plan in Spain.

Pro Tip: Registering for a NIE (Número de Identificación de Extranjero) or signing up at your local padrón does not make you a tax resident. These are administrative steps. Fiscal residency is determined by real living circumstances and actual physical presence, not paperwork alone.

There is a critical distinction between administrative residency and fiscal residency that trips up many expats. Your NIE proves your legal right to be in Spain. Your padrón registration proves you live at a specific address in a specific municipality. Neither document alone establishes fiscal residency for tax purposes. Fiscal residence requires meeting the criteria under tax law and demonstrating physical presence and economic connection through verifiable evidence.

How do regional residency rules differ from national ones?

Regional residency in Spain, governed by Article 72 LIRPF, operates on a strict hierarchical system that is fundamentally different from the inclusive national criteria. Where national rules say "meet any one criterion," regional rules say "apply criterion one first, and only move to criterion two if criterion one does not resolve the question." The hierarchy works as follows: physical presence in the autonomous community comes first, center of economic interests comes second, and last declared fiscal residence comes third as a fallback.

This hierarchy matters enormously in practice. If you spend 120 days in Madrid and 80 days in Barcelona during a tax year, the physical presence criterion assigns you to Madrid. The economic interests criterion never even enters the calculation. Only when physical presence is genuinely split or impossible to determine does the system move to the next level.

The financial stakes of regional assignment are substantial. The table below illustrates the key differences between selected autonomous communities as of 2026.

| Autonomous community | Net Wealth Tax | Inheritance and Gift Tax | Housing residency requirement |

|---|---|---|---|

| Madrid | 100% bonus (effectively zero) | Significant regional reductions | Standard padrón registration |

| Catalonia | Full liability applies | Full rates apply | Standard padrón registration |

| Valencia | Full liability applies | Full rates apply | Standard padrón registration |

| Balearic Islands | Full liability applies | Full rates apply | Standard padrón registration |

| Castilla y León | Standard rates | Standard rates | 10 years for protected housing |

Madrid's full tax exemption on Net Wealth Tax is offset by state transfers to the central government, but residents still pay nothing directly. This is why Madrid has become the preferred destination for wealthy relocators from across Europe and Latin America.

Pro Tip: If you are considering moving between autonomous communities to reduce your tax burden, be aware that inter-regional moves face scrutiny if the new residency lasts fewer than three years and your tax liability drops substantially. The Agencia Tributaria can challenge the move and deny the tax benefit entirely.

What practical implications do these distinctions have for expats?

The split between national and regional residency rules creates two separate sets of obligations that you must satisfy simultaneously. National residency triggers your obligation to file an annual IRPF (income tax) return covering worldwide income. Regional residency determines which autonomous community receives the regional share of that tax, and which community's rates apply to your wealth and inheritance taxes.

For most expats, the most immediate practical impact falls into three areas:

- Net Wealth Tax and Inheritance Tax. These taxes are almost entirely managed at the regional level. A person with 2 million euros in assets pays nothing in Net Wealth Tax if registered in Madrid, but faces a significant bill in Catalonia or Valencia. The regional tax differences also trigger differing legal disputes when residents attempt to change their autonomous community registration to access lower rates.

- Padrón registration and fiscal proof. The padrón is the municipal census register. Padrón registration is not legally required under EU residency decrees, but it is routinely demanded in practice for everything from opening a bank account to enrolling children in school. Critically, it does not prove fiscal residency. The Agencia Tributaria looks at actual physical presence, utility bills, school records, and bank statements.

- Access to regional services. Regional residency is not just about taxes. Castilla y León now requires 10 years of residency to purchase protected housing and 5 years to access social rent. This kind of requirement is set entirely at the regional level and varies significantly across Spain's 17 autonomous communities.

A common misconception among expats is that registering at the padrón in a low-tax region immediately establishes regional fiscal residency there. It does not. Fiscal residency depends on real living circumstances, not just formal registrations or place of work. If you register in Madrid but spend most of your time in Barcelona, the Agencia Tributaria will assign you to Catalonia based on physical presence. You can also read more about how tax burden shifts when UK citizens relocate to Spain for a concrete example of how these rules play out.

How to comply with both national and regional residency requirements

Satisfying both layers of Spain's residency framework requires deliberate documentation from the moment you arrive. Follow these steps to establish and maintain compliant residency.

- Track your physical presence from day one. Keep a dated log of your entries and exits from Spain and from each autonomous community. Flight records, hotel receipts, and credit card statements all serve as evidence. The 183-day national threshold and the regional physical presence criterion both depend on this data.

- Register at the padrón promptly. Even though padrón registration does not establish fiscal residency, it creates an official record of your address and start date in a specific municipality. Register within 30 days of arriving at your permanent address. This record will be requested repeatedly throughout your time in Spain.

- Obtain your NIE and TIE. The NIE (tax identification number) is required for almost every financial transaction in Spain. The TIE (Tarjeta de Identidad de Extranjero) is the physical residency card issued after your visa is approved. Neither establishes fiscal residency, but both are required for the administrative side of your life in Spain.

- File your first IRPF return correctly. Your first tax return in Spain establishes your fiscal residency on record. The autonomous community you declare must match your actual physical presence during the tax year. Mismatches between your padrón address and your declared fiscal residence are a common audit trigger.

- Document your economic ties to the region. Bank accounts, investment portfolios, business registrations, and property ownership all support your regional fiscal residency claim. If your economic interests are split across regions, the hierarchy under Article 72 LIRPF moves to the next criterion.

Pro Tip: If you split time between two autonomous communities and cannot clearly establish majority physical presence in one, consult a Spanish tax advisor before filing your first return. The fallback criterion of "last declared residence" can produce unexpected results, and correcting a misassignment after the fact is significantly harder than getting it right the first time.

For non-EU nationals, the residency pathway itself adds another layer. Your visa type, whether a Non-Lucrative Visa, Digital Nomad Visa, or partner residency, determines your initial legal status in Spain. That legal status then feeds into the national and regional fiscal residency determination. Understanding Spain's pareja de hecho requirements is one example of how legal and fiscal residency interact for couples relocating together.

Key takeaways

Spain's residency framework requires satisfying both national criteria under Article 9 LIRPF and regional criteria under Article 72 LIRPF, and the two systems use different logic that produces different legal and financial outcomes.

| Point | Details |

|---|---|

| National criteria are inclusive | Meeting any one of the three Article 9 LIRPF criteria makes you a Spanish tax resident. |

| Regional criteria are hierarchical | Article 72 LIRPF applies physical presence first, then economic interests, then last declared residence. |

| Tax stakes are region-specific | Madrid's 100% Net Wealth Tax bonus versus full liability in Catalonia or Valencia can mean tens of thousands of euros annually. |

| Padrón ≠ fiscal residency | Administrative registration proves your address, not your tax status. Real evidence of physical presence is decisive. |

| Inter-regional moves face scrutiny | Residency changes that reduce tax liability are presumed ineffective if the new residency lasts fewer than three years. |

Why most expats get this wrong until it costs them

Most people moving to Spain treat residency as a single checkbox. Get the visa, register at the padrón, done. That mental model is accurate for administrative purposes and dangerously incomplete for fiscal ones.

What I see repeatedly, working with clients at Epic-residency, is that the national versus regional distinction only becomes visible when something goes wrong. A client registers in Madrid, spends most of their first year traveling between Madrid and their vacation property in Mallorca, and then discovers at tax time that the Agencia Tributaria has assigned them to the Balearic Islands based on physical presence. The padrón said Madrid. The tax authority said Balearics. The client paid full Net Wealth Tax when they thought they had a 100% exemption.

The uncomfortable truth is that Spain's dual residency system rewards people who treat it as a compliance project from day one, not an afterthought. That means logging your days, documenting your economic ties, and understanding that the region where you spend the most time is almost always the region that will claim you, regardless of where you registered. The property tax obligations that come with owning real estate in Spain add yet another dimension to this, particularly for people who own property in a different region from where they live.

The clients who navigate this well are the ones who ask the right questions before they move, not after their first tax return lands.

— Living

How Epic-residency helps you get residency right from the start

Spain's dual residency framework is manageable when you have the right guidance from the beginning. Epic-residency is a boutique Spain-focused immigration and relocation consultancy that specializes in exactly this kind of complexity. Whether you are applying for a Non-Lucrative Visa, a Digital Nomad Visa, or a partner residency, Epic-residency maps your specific situation against both national and regional criteria before you file a single document. The team handles visa applications, padrón strategy, and tax residency planning as a connected process, not three separate tasks. If you are planning a move to Spain and want clarity on how regional and national rules apply to your circumstances, contact Epic-residency for a personalized consultation.

FAQ

What is the difference between national and regional residency in Spain?

National residency under Article 9 LIRPF determines whether you are a Spanish tax resident at all, based on physical presence, economic interests, or family ties. Regional residency under Article 72 LIRPF determines which autonomous community claims you, using a strict hierarchy of physical presence first, economic interests second, and last declared residence third.

Does padrón registration prove fiscal residency in Spain?

No. Padrón registration is an administrative record of your address and is not legally sufficient to establish fiscal residency. The Agencia Tributaria determines fiscal residency based on actual physical presence, economic ties, and other verifiable evidence of real living circumstances.

Can I choose which autonomous community I am a tax resident of?

You cannot freely choose your regional fiscal residency. The hierarchical criteria under Article 72 LIRPF assign you based on where you actually spend the most time. Attempts to register in a low-tax region like Madrid while living elsewhere are subject to challenge, and moves that reduce tax liability by more than a threshold amount are presumed ineffective if the new residency lasts fewer than three years.

How does regional residency affect my taxes in Spain?

Regional residency determines your liability for Net Wealth Tax and Inheritance and Gift Tax, which vary dramatically across Spain's autonomous communities. Madrid applies a 100% bonus on Net Wealth Tax, effectively eliminating it, while Catalonia, Valencia, and the Balearic Islands apply full rates.

What documents do I need to prove residency in Spain?

You need a combination of administrative documents (NIE, TIE, padrón certificate) and evidence of real physical presence such as utility bills, bank statements, school enrollment records, and travel records. Administrative documents alone are not sufficient for fiscal residency purposes.