Spain's Non-Lucrative Visa (NLV) requires applicants to prove stable passive income or liquid savings before a single document reaches the consulate. The spain long term visa income sources that qualify are specific: pensions, dividends, rental income, annuities, royalties, and investment returns. Active income, freelance earnings, and remote work pay do not qualify. The minimum annual threshold is €28,800 for the main applicant, plus €7,200 per dependent, calculated at 400% of Spain's IPREM benchmark. Get this wrong and your application fails before the consulate reviews anything else.

What counts as acceptable passive income for Spain's Non-Lucrative Visa?

Passive income, in the Spanish visa context, is income that arrives without you actively working for it. The Spanish consulate expects that income to be non-contingent on active work and reliably recurring. That distinction matters more than most applicants realize.

The accepted passive income sources include:

- Pensions. State pensions, private pensions, and annuities all qualify. You need an official pension award letter showing the monthly or annual amount.

- Dividends. Dividend income from stocks or business ownership qualifies, provided you are not actively managing the company. Brokerage statements or dividend distribution records are required.

- Rental income. Income from residential or commercial property leases qualifies. You need signed lease agreements and bank records showing regular deposits.

- Annuities and royalties. Structured annuity payments and royalty income from intellectual property both qualify. Official statements from the paying institution are required.

- Investment returns. Returns from bonds, mutual funds, or managed portfolios qualify. Brokerage account statements showing consistent distributions work as proof.

Salaried employment income, freelance contracts, and remote work pay do not qualify under the NLV. The visa is explicitly designed for people who do not need to work in Spain. If your income comes from a job, even a foreign one, the NLV is not your path. The Digital Nomad Visa exists specifically for remote workers.

Pro Tip: Business owners who receive dividends must prove they are silent partners with no day-to-day operational role. A notarized CPA letter confirming zero active management duties is required. Without it, the consulate treats dividend income as active business income and rejects it.

How to calculate the minimum income threshold for your application

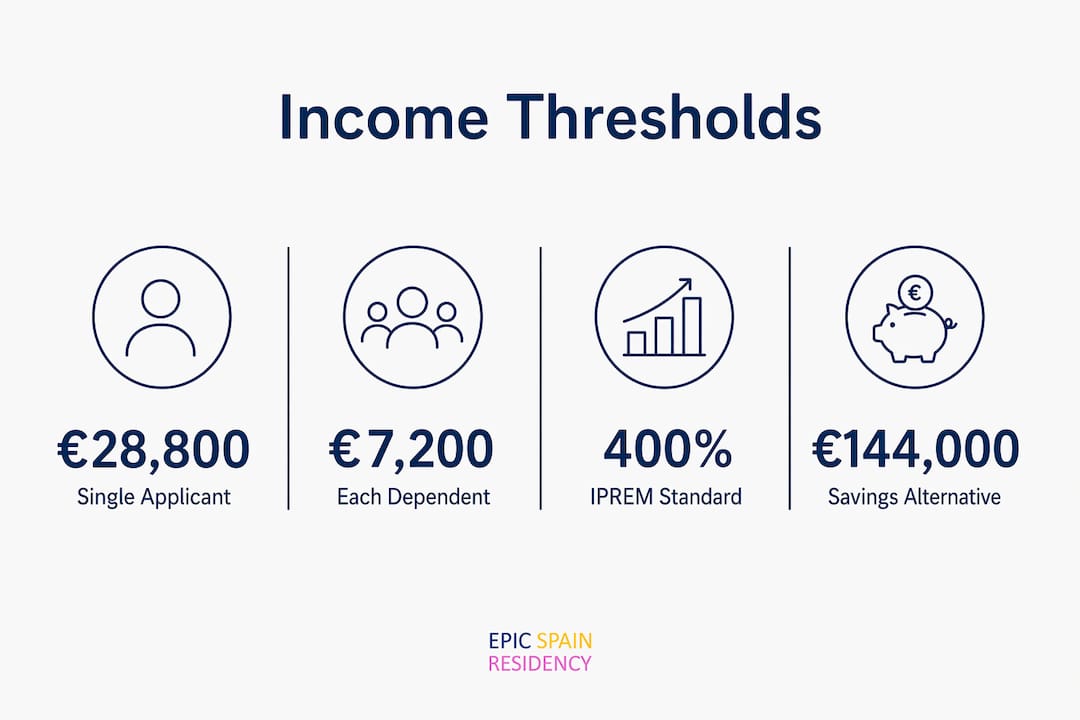

The IPREM (Indicador Público de Renta de Efectos Múltiples) is Spain's public income reference index. The NLV requires income equal to 400% of the annual IPREM. The current monthly IPREM figure is €600, making the annual IPREM €7,200. Four hundred percent of that equals €28,800 per year for the main applicant.

Each dependent you bring adds €7,200 per year to the requirement. The table below shows the total annual income needed by family size.

| Family size | Annual income required |

|---|---|

| 1 applicant (no dependents) | €28,800 |

| 1 applicant + 1 dependent | €36,000 |

| 1 applicant + 2 dependents | €43,200 |

| 1 applicant + 3 dependents | €50,400 |

If your passive income does not reach the threshold, liquid savings can substitute. Many applicants show savings rather than recurring income. The common strategy is to demonstrate five years of funds upfront. For a single applicant, that means showing approximately €144,000 in accessible savings. That figure reassures the consulate that you can sustain yourself through the initial visa period and two renewals without needing to work.

One critical detail: not all assets count as liquid savings. Real estate equity, cryptocurrencies, and locked retirement funds are generally not accepted. The consulate wants to see cash or near-cash assets in bank accounts you can access immediately.

How to document and prove your income sources

Gathering the right documents is where most applications succeed or fail. Each income type has its own documentation standard, and the consulate checks for consistency across all of them.

- Pension income. Request an official pension award letter from your pension provider or government agency. The letter must state the annual or monthly amount and be dated within three months of your application.

- Dividend income. Provide at least 12 months of brokerage statements showing regular dividend distributions. If you own shares in a private company, include the notarized CPA letter confirming your silent partner status.

- Rental income. Submit signed lease agreements, three to six months of bank statements showing rental deposits, and proof of property ownership such as a title deed.

- Investment returns. Provide brokerage or fund manager statements covering 6–12 months. The statements must show your name, account number, and consistent distributions.

- Savings as substitute. Submit 3–6 months of bank statements showing the full balance. The balance must be stable throughout, not a recent spike.

All documents in a language other than Spanish require certified translation. Certified translations of complex financial documents from official entities improve approval chances by removing any ambiguity about figures or terms. Use a sworn translator recognized by the Spanish Ministry of Foreign Affairs, not a generic translation service.

Pro Tip: Consulates flag sudden large deposits as red flags. A stable financial history over 6–12 months is far more persuasive than a large transfer made weeks before applying. If you plan to consolidate funds, do it at least a year before submitting.

The most common rejection trigger is misclassifying active income as passive. Applicants who receive consulting fees, freelance payments, or director salaries and try to present them as investment income consistently get rejected. Clear evidence of labor detachment is non-negotiable.

For a full breakdown of what each consulate accepts, the Spain visa financial proof guide covers documentation standards in detail.

How do income requirements change after your initial visa approval?

The NLV is issued for one year and renewed in two-year increments. At each renewal, you must show continued passive income or savings meeting the same IPREM-based threshold. The financial bar does not drop during the renewal phase. You still need to prove you are not working in Spain and that your income remains passive and sufficient.

The picture changes significantly after five years. Once you qualify for long-term residency, known in Spain as "larga duración," the strict income thresholds lift. No specific income amount is required at that stage. Work restrictions also disappear entirely. You can take employment, run a business, or freelance without any visa condition preventing it.

That transition is the real prize for NLV holders. The five-year path converts a passive-income-only residency into full long-term status with near-equal rights to Spanish citizens. Planning your finances around that timeline, rather than just the first year, is the smarter approach. Applicants who understand the family reunification implications of long-term residency are better positioned to plan for dependents at each stage.

At renewal, you will also need to show proof of private health insurance with full coverage in Spain. That cost adds to your living expenses and should factor into your financial planning from day one.

Key Takeaways

Qualifying for Spain's Non-Lucrative Visa requires passive income of at least €28,800 per year, documented consistently, with no active work income included.

| Point | Details |

|---|---|

| Minimum income threshold | €28,800 per year for one applicant; add €7,200 for each dependent. |

| Accepted income types | Pensions, dividends, rental income, annuities, royalties, and investment returns all qualify. |

| Active income is excluded | Salaries, freelance pay, and remote work income do not qualify under the NLV rules. |

| Savings as an alternative | Showing approximately €144,000 in liquid savings covers a single applicant for five years. |

| Long-term residency shift | After five years, income thresholds and work restrictions no longer apply under "larga duración" status. |

What I have learned about financial preparation for Spain visa applicants

The biggest mistake I see is applicants treating the income threshold as a box to check rather than a case to build. Consulates are not just verifying a number. They are assessing whether your financial life is genuinely passive and stable. That requires a story told through consistent documents, not a last-minute scramble.

Applicants who show five years of financial stability, rather than the bare minimum for one year, get far fewer requests for additional evidence. That 5-year savings approach is not required, but it signals confidence and reduces back-and-forth with the consulate. It also protects you if your passive income dips in year two or three.

Diversifying your income sources also helps. An applicant showing a pension plus rental income plus dividends is more convincing than one relying on a single source. Each stream reinforces the others and demonstrates that your financial position is not fragile.

Professional document preparation and certified translation are not optional extras. I have seen strong applications rejected because a pension letter was translated by an uncertified service or because a brokerage statement lacked the account holder's name on every page. The consulate has no obligation to ask for clarification. It simply declines.

— Living

How Epic-residency helps you meet Spain's income proof requirements

Preparing a financially airtight NLV application takes more than gathering bank statements. Epic-residency works directly with applicants to organize, verify, and present income documentation in the format each consulate expects.

Epic-residency's team reviews your income sources, identifies documentation gaps before submission, and coordinates certified translations through approved translators. For business owners navigating silent partner documentation, the process is especially detailed. If you are ready to build a strong financial case for your Non-Lucrative Visa application, Epic-residency offers a consultation to assess your income profile and map out exactly what you need.

FAQ

What income sources qualify for Spain's Non-Lucrative Visa?

Pensions, dividends, rental income, annuities, royalties, and investment returns all qualify. Salaries, freelance income, and remote work pay do not.

How much passive income do I need for the Spain NLV?

The minimum is €28,800 per year for the main applicant, plus €7,200 for each dependent, based on 400% of Spain's IPREM.

Can I use savings instead of regular passive income?

Yes. Liquid savings in an accessible bank account can substitute for recurring income. Showing approximately €144,000 covers a single applicant for five years.

Do income requirements change at visa renewal?

No. You must meet the same IPREM-based threshold at each renewal until you qualify for long-term residency after five years, at which point income restrictions lift.

Why do consulates reject passive income claims from business owners?

Consulates reject dividend income if the applicant appears to be actively managing the business. A notarized CPA letter confirming silent partner status is required to prove the income is genuinely passive.