Many UK business owners assume that drawing income from a UK company automatically qualifies them for Spanish residency. It does not. Spain's visa system is specific about income sources, amounts, and how that income is structured. Whether you run a limited company, work remotely for a UK employer, or take dividends as your primary income, each scenario lands you in a different visa category with different rules. Getting this wrong is one of the most common reasons UK applicants face delays or outright rejections. This guide breaks down exactly how UK company income spain visa eligibility works in 2026.

Table of Contents

- Key Takeaways

- UK company income spain visa eligibility: the visa types that matter

- Income thresholds and proof requirements

- Tax and payroll implications for UK company owners

- Common application challenges and how to avoid them

- Practical steps for applying and maintaining residency

- My take on what UK business owners consistently get wrong

- How Epic-residency helps UK business owners move to Spain

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Visa type determines income rules | Different visas treat UK company income differently, so choosing the right route matters before you apply. |

| Digital Nomad Visa income threshold | Single applicants must show at least €2,849 per month from a foreign employer or client in 2026. |

| Non-lucrative visa bars active work | This visa requires passive income around €28,800 per year and prohibits working for Spanish clients. |

| Beckham Law timing is critical | You must apply within six months of arrival to access Spain's 24% flat tax rate on employment income. |

| Documentation quality decides outcomes | Translated, apostilled, and complete financial records are what separate approvals from rejections. |

UK company income spain visa eligibility: the visa types that matter

Spain does not offer a single "business income visa." Instead, UK company owners must identify which existing visa category fits their income structure. Three routes dominate the conversation.

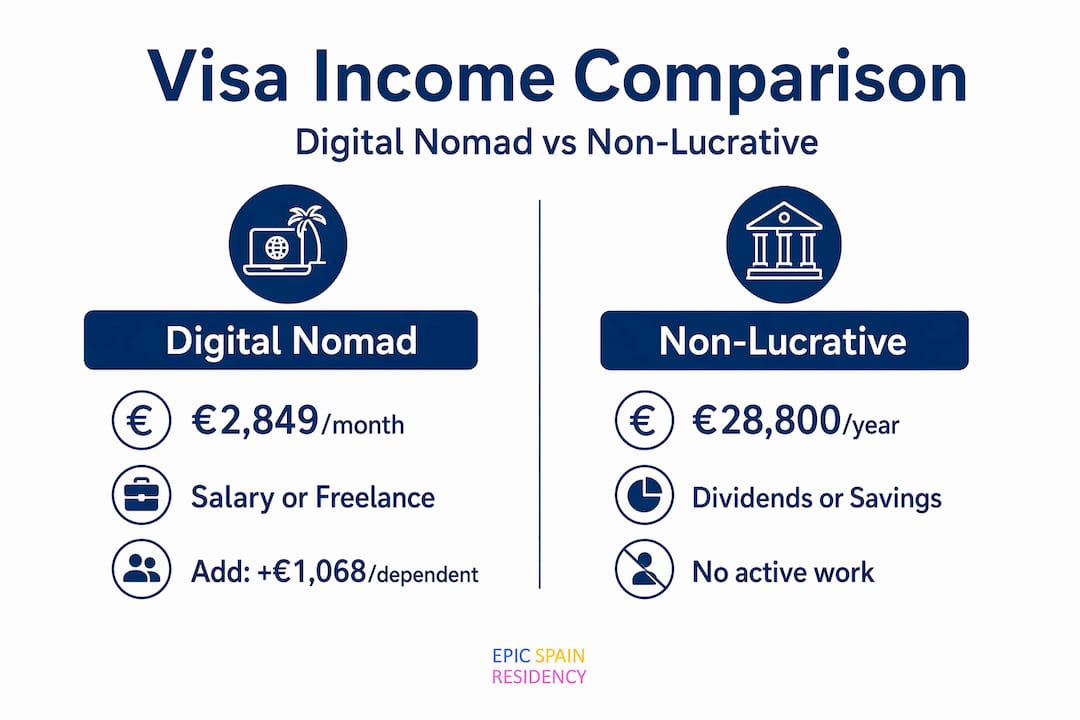

The Non-Lucrative Visa (NLV) is the most commonly misunderstood option. It allows you to live in Spain without working in the country, funded by passive income or savings. Dividends from a UK company can qualify here, but only if you are not actively managing the company from Spain in a way that generates new income. The non-lucrative visa requires proof of stable, passive income rather than salary.

The Digital Nomad Visa (DNV) is the better fit for UK business owners who are employed by or contracted to a UK company and work remotely. This visa specifically targets people earning income from foreign sources while living in Spain. Importantly, foreign source income is the defining requirement. If you receive a salary from a UK employer, that qualifies. If you invoice a UK company as a freelancer, that can also qualify, though the documentation requirements differ.

Spanish Work Permits apply when you want to work for a Spanish employer or set up a Spanish entity. This route is less relevant for most UK company owners unless they plan to hire locally or establish a Spanish branch.

Here is a quick comparison of how each visa treats UK company income:

- Non-Lucrative Visa: Passive income only. Dividends and investment returns from UK companies can qualify. Active management from Spain is a gray area that consulates scrutinize carefully.

- Digital Nomad Visa: Salary or freelance income from a UK company qualifies. You must be employed or contracted by a foreign entity and can work for Spanish clients only up to 20% of your total income.

- Spanish Work Permit: Requires a Spanish employer contract. UK company income is not relevant here unless that UK company registers a payroll in Spain.

Income thresholds and proof requirements

Spain's income thresholds are not arbitrary numbers. They are tied to official wage benchmarks and adjusted regularly, which means what qualified you last year may not qualify you today.

For the Digital Nomad Visa in 2026, a single applicant must demonstrate at least €2,849 per month. Add a dependent partner and that figure rises by €916 per month. Each additional dependent child adds another €305 per month. These figures are indexed to the Spanish minimum wage, which the government adjusts through annual Real Decreto legislation. The income requirement indexation means you need to verify current thresholds close to your application date, not months in advance.

For the Non-Lucrative Visa, the benchmark sits at roughly €28,800 per year for a single applicant. This can be demonstrated through savings, investment returns, pension income, or dividends. Bank statements covering the previous six to twelve months are standard. Consulates want to see consistency, not a lump sum that appeared recently.

| Visa Type | Single Applicant Minimum | First Dependent | Income Source |

|---|---|---|---|

| Digital Nomad Visa | €2,849/month | +€916/month | Foreign employer or client |

| Non-Lucrative Visa | ~€2,400/month (€28,800/year) | +20% per dependent | Passive income or savings |

| Spanish Work Permit | Varies by role | N/A | Spanish employer payroll |

Proof requirements are where many applications fall apart. Consulates expect bank statements, payroll slips or dividend certificates, employment contracts or client agreements, and tax returns from the previous year. All documents must be translated into Spanish by a certified translator and, if issued in the UK, accompanied by an apostille stamp.

Pro Tip: Request your apostilled documents at least six weeks before your application appointment. Post-Brexit processing times at the UK Foreign, Commonwealth and Development Office have extended, and delays here can push back your entire timeline.

Tax and payroll implications for UK company owners

Moving to Spain does not end your relationship with UK tax rules. It complicates it. Understanding how your UK company income interacts with Spanish tax residency is not optional. It is the difference between a tax-efficient move and an expensive mistake.

Spain's Beckham Law is the headline benefit most UK expats hear about. It offers a 24% flat tax rate on Spanish employment income up to €600,000 for qualifying expats. For UK nationals employed by a UK company who relocate to Spain, this can be genuinely attractive. The catch is timing. You must apply within six months of registering as a Spanish tax resident. Miss that window and the benefit is gone permanently for that residency period.

The Beckham Law applies to employed workers. If you receive a salary from your UK company under a formal employment contract, you likely qualify. If you take dividends only, or work as a self-employed contractor, you generally do not. This distinction catches many UK limited company directors off guard.

There are also employer-side obligations worth knowing:

- UK companies with employees physically working in Spain may need to register for Spanish payroll and Social Security, even if the company has no Spanish office.

- Failure to register can expose both the employer and employee to back taxes and penalties.

- The UK-Spain double taxation treaty provides relief in many cases, but it does not eliminate the need for proper registration.

Pro Tip: If you are considering the Beckham Law, speak to a cross-border tax advisor before you arrive in Spain, not after. The tax reduction strategies available to UK expats depend heavily on how your income is structured before you become a Spanish tax resident.

The Beckham Law's application window being limited to six months is not a technicality. It is a hard deadline that Spanish tax authorities enforce without exception.

Common application challenges and how to avoid them

The most frequent reason Spanish visa applications fail is not that the applicant lacks the income. It is that they cannot prove it convincingly. Incomplete or unverified income documentation is among the top causes of rejection across all visa categories.

For UK company owners, the documentation challenge is more complex than for salaried employees. Dividends require company accounts. Freelance income requires contracts and invoices. Directors' loans or irregular drawings raise red flags. Consulates want to see a clean, consistent income story across your bank statements, tax returns, and supporting documents.

Several specific pitfalls affect UK applicants more than others:

- Post-Brexit document requirements: UK documents no longer benefit from EU mutual recognition. Every official document needs an apostille, and many consulates now require notarized translations even for standard financial records.

- Irregular income patterns: If your UK company income fluctuates significantly month to month, you need to demonstrate an average that meets the threshold consistently over at least six months.

- Mixing income sources: Some applicants combine salary, dividends, and rental income to meet thresholds. This is acceptable, but each source needs its own documentation chain.

- Applying for the wrong visa: A director taking dividends applying for a Digital Nomad Visa will likely be rejected because dividends do not constitute employment income from a foreign employer.

- Underestimating consulate discretion: Spanish consulates in different cities can interpret income rules slightly differently. The consulate serving your UK region matters.

The solution in every case is the same: thorough, translated, apostilled documentation that tells a consistent financial story before the consulate asks a single question.

Practical steps for applying and maintaining residency

Getting the visa is step one. Keeping it requires ongoing compliance. Here is how to approach both.

- Identify your correct visa category before gathering any documents. Your income structure, whether salary, dividends, or freelance contracts, determines which route applies.

- Calculate your income requirement including any dependents. Use the current thresholds, not last year's figures, since the Digital Nomad Visa threshold changes with the Spanish minimum wage.

- Gather six to twelve months of bank statements showing consistent income deposits that match your declared sources.

- Obtain apostilles for all UK-issued documents including company accounts, employment contracts, and tax returns.

- Commission certified Spanish translations for every document. This is not optional and cannot be done by a bilingual friend.

- Apply for the Beckham Law within six months of arriving and registering as a tax resident if you qualify as an employed worker.

- Track your physical presence in Spain. Residency renewal requires more than 183 days of physical presence in Spain per calendar year. Falling below this risks losing your residency status.

- Update your income proof at renewal with fresh bank statements and tax filings. Consulates do not accept documents older than three months at the renewal stage.

- Review your UK tax position annually. Becoming a Spanish tax resident affects your UK tax status, and the interaction between the two systems requires active management.

- Consult a specialist before major decisions. Visa rules, tax treaties, and income thresholds all shift. Working with people who track these changes professionally is not a luxury. It is risk management.

My take on what UK business owners consistently get wrong

I have worked with enough UK company owners going through this process to recognize the pattern. They arrive well-prepared financially and completely underprepared documentarily. They have the income. They cannot prove it in the format Spain requires.

The second consistent mistake is treating the visa as the finish line. Spain's residency policy evolves. Income thresholds move. Tax rules shift. The people who settle successfully in Spain are the ones who treat their residency as an ongoing compliance project, not a one-time application.

I also think the Beckham Law gets oversold. It is a genuinely useful benefit for the right person, but the six-month application window and the employment contract requirement mean it does not apply to most UK limited company directors taking dividends. If your income structure does not fit the criteria before you move, restructuring it after you arrive is often too late.

What actually works is pre-move planning. Restructuring your income, getting your documentation in order, understanding which visa category fits your situation, and timing your arrival to maximize tax benefits. None of this is complicated once you understand the rules. The problem is that most people discover the rules after they have already made decisions that are hard to reverse.

— Epic-residency

How Epic-residency helps UK business owners move to Spain

Figuring out which visa fits your income structure, gathering the right documents, and staying compliant after you arrive is genuinely complex. Epic-residency specializes in exactly this.

Epic-residency is a boutique Spain immigration consultancy that works with UK nationals and other non-EU individuals navigating the full range of Spanish residency options. Whether you are exploring the non-lucrative visa as a dividend-income earner, or the Digital Nomad Visa as a remotely employed UK worker, the team handles documentation, consulate preparation, and post-arrival compliance. Epic-residency also supports families with partner visas and rental transitions, so your entire relocation is covered. If you want to see how other UK nationals have made this work, the client case studies are worth reading before you start your own application.

FAQ

What income qualifies for UK company income Spain visa eligibility?

It depends on the visa. Dividends from a UK company can support a Non-Lucrative Visa application, while a salary or freelance contract from a UK employer qualifies for the Digital Nomad Visa. The income source must match the visa category.

How much income do I need for Spain's Digital Nomad Visa in 2026?

A single applicant needs at least €2,849 per month from a foreign employer or client. This figure increases with each dependent added to the application.

Can I use dividend income from my UK company to qualify?

Yes, but only for the Non-Lucrative Visa, which requires roughly €28,800 per year and prohibits active work in Spain. Dividends do not qualify as employment income for the Digital Nomad Visa.

Does the Beckham Law apply to UK company directors?

Generally no. The Beckham Law flat rate applies to employed workers with formal contracts. Directors who take dividends rather than salary typically do not qualify.

What documents do UK applicants need to prove income for a Spanish visa?

You will need bank statements, payroll slips or dividend certificates, employment contracts or client agreements, and your most recent tax return. All documents must be apostilled and translated into Spanish by a certified translator.