UK savings Spain visa eligibility is determined by Spain's Non-Lucrative Residence Visa (NLV) financial threshold, which requires the main applicant to demonstrate €28,800 in annual funds for 2026. This figure is not arbitrary. It is calculated as 400% of Spain's IPREM index, the official public income reference used across Spanish immigration law. For UK nationals planning to move to Spain after Brexit, understanding this threshold is the foundation of every successful application. Your UK savings accounts, pension income, and investment dividends can all count toward this requirement, but only if you present them correctly to the Spanish consulate.

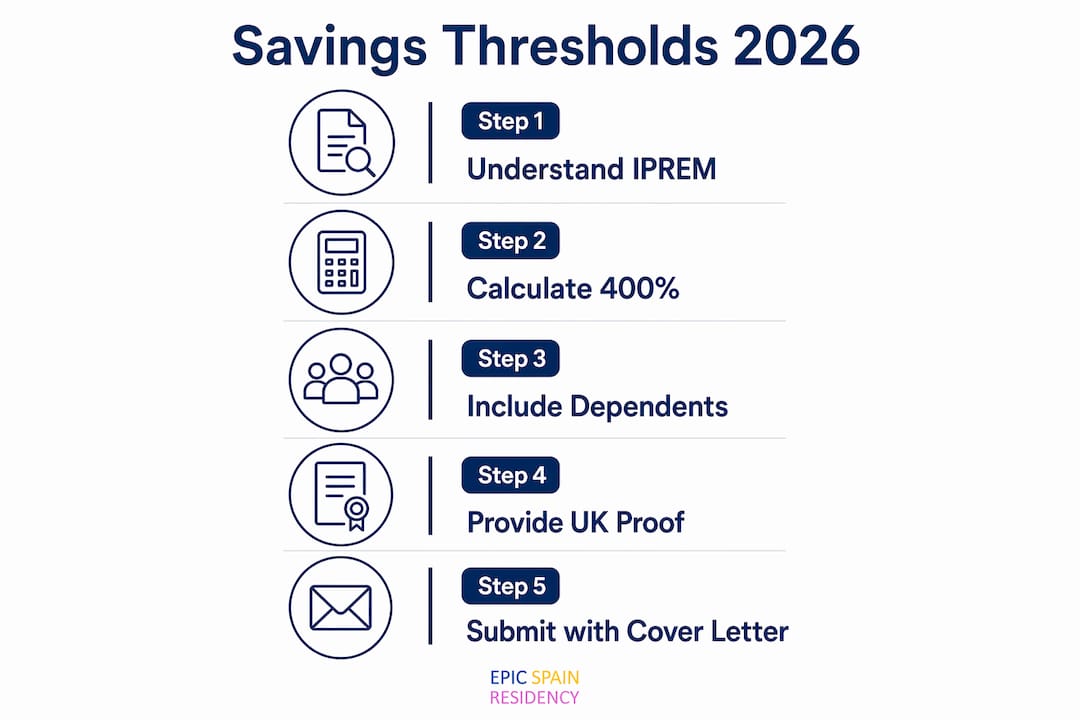

What is the IPREM and how does it set your savings threshold?

The IPREM (Indicador Público de Renta de Efectos Múltiples) is Spain's official public income benchmark, used by courts, social services, and immigration authorities to set financial eligibility thresholds. In 2026, the IPREM stands at €600 per month, or €7,200 per year. That number alone tells you nothing useful. What matters is how Spanish immigration law multiplies it.

Under Artículo 62 del Reglamento de Extranjería, the main applicant must show 400% of the annual IPREM, which equals €28,800 per year. Each dependent added to the application, whether a spouse or child, requires an additional 100% IPREM per year, or €7,200. The table below shows how this scales for common family situations.

| Applicant type | Annual requirement (2026) |

|---|---|

| Single applicant | €28,800 |

| Couple (main + 1 dependent) | €36,000 |

| Family of 3 (main + 2 dependents) | €43,200 |

| Family of 4 (main + 3 dependents) | €50,400 |

The required funds are tied to the duration of the residency authorization, so you calculate the total based on the visa period you are applying for. A one-year initial NLV means you need to demonstrate the full annual amount upfront.

Pro Tip: Do not confuse monthly income with total savings. Consulates want to see that your total accessible funds cover the full authorization period, not just that you receive a monthly amount that would theoretically add up.

How can UK savings documents prove your Spain visa eligibility?

Spanish consulates accept several forms of financial evidence from UK applicants. The key is demonstrating that your funds are real, accessible, and stable. Accepted sources include:

- UK savings account balances shown via official bank statements from institutions like Barclays, HSBC, Lloyds, or NatWest

- Pension income from UK state pension, workplace pensions, or private pension drawdown statements

- Investment dividends from UK-based portfolios, shown via annual dividend statements or broker account summaries

- Rental income from UK properties, supported by tenancy agreements and bank deposits

- Certified bank balances as of December 31 of the prior year, or average balances over the preceding 12 months

Consulates accept balances at December 31 and average balances over the past year as valid evidence. This means a single high-balance snapshot can work, but a 12-month average is often more persuasive because it demonstrates consistency rather than a one-time transfer.

Every document from a UK institution must be apostilled under the Hague Convention and accompanied by a certified Spanish translation. A statement from Barclays means nothing to a consular officer in Madrid unless it carries an apostille stamp and a sworn translation. Budget time for this. Apostilles from the UK Foreign, Commonwealth and Development Office typically take one to two weeks, and certified translators add another layer of lead time.

Pro Tip: Include a cover letter summarizing all income sources and their corresponding documents. A summary cover letter listing each source greatly aids consulate officers reviewing your application, and it signals that you understand the process.

What are the common pitfalls UK applicants face with savings proof?

Most rejections or delays on the NLV do not come from applicants who are genuinely underfunded. They come from applicants who present their funds poorly. Four specific mistakes account for the majority of problems.

-

Depositing a large lump sum shortly before applying. Consulates scrutinize fund availability over time using average balances and past statements. A £40,000 transfer that appeared in your account three weeks before the application date raises red flags. Funds should have been sitting in your account for at least six to twelve months.

-

Meeting only the minimum threshold. Applicants who meet only minimum amounts may face additional documentation requests. Consulates sometimes interpret marginal funds as a risk indicator, especially when savings are the primary source rather than steady pension or investment income. Aim for at least 10 to 20 percent above the minimum.

-

Ignoring consulate-specific requirements. Spanish consulates in London, Manchester, and Edinburgh interpret savings proofs differently. What satisfies the London consulate may not satisfy Edinburgh. Check the specific requirements of the consulate with jurisdiction over your UK postcode before preparing your documents.

-

Misunderstanding the work prohibition. The NLV prohibits working in Spain, including remote work for foreign employers. This matters for financial proof because if you plan to supplement your savings with freelance income while in Spain, the NLV is the wrong visa category. Consulates will assess whether your stated financial means are genuinely passive.

"The Non-Lucrative visa is designed for people who can live in Spain without working. If your financial plan depends on earning income once you arrive, you need a different visa. Presenting a financial package that implies future earnings rather than existing means is one of the fastest ways to get rejected." — Non-Lucrative Visa Spain 2026

How does UK residency status affect your savings accounts and eligibility?

Moving to Spain changes your UK tax residency status, and that change has direct consequences for the savings and investment accounts you plan to use as financial proof. Understanding these effects before you apply prevents nasty surprises.

- UK ISAs: Existing ISAs remain open but cannot receive new contributions once you become non-resident. Your ISA balance continues to grow tax-free, and you can use the balance as savings evidence for your NLV application. You simply cannot add new money to it after you leave the UK.

- UK investment platforms: Most UK retail investment platforms restrict account opening to UK residents, but existing accounts can usually be kept. Specialist platforms like AJ Bell International are built specifically for non-resident UK nationals and allow continued portfolio management from abroad.

- Dividend and interest income: UK investment income and dividend treatment changes under non-residency status, which affects the net income figure you can legitimately present as proof. UK dividends paid to non-residents may be subject to withholding tax under the UK-Spain double taxation treaty, reducing the net amount available to show consulates.

- Pension income: UK state pension and private pension income remains accessible to non-residents and is one of the cleanest forms of financial proof for the NLV. Pension statements are straightforward to apostille and translate.

The strategic implication is clear. Plan your financial structure before you apply, not after. If you hold a Stocks and Shares ISA with a significant balance, document it thoroughly before your residency status changes. If you rely on dividend income, calculate the post-withholding net figure and check whether it still meets the IPREM threshold. You can also read more about tax implications of moving to Spain as a UK national to understand how your overall financial picture shifts.

Key takeaways

Meeting Spain's NLV financial threshold requires €28,800 per year for a single UK applicant in 2026, with each dependent adding €7,200, and the strongest applications combine consistent 12-month savings history with a financial buffer above the minimum IPREM multiple.

| Point | Details |

|---|---|

| Core savings threshold | Single applicants need €28,800/year in 2026, calculated as 400% of Spain's IPREM. |

| Dependent costs | Each dependent adds €7,200/year to the required total under Artículo 62. |

| Document consistency | Show 12 months of stable balances, not a single large recent deposit. |

| Build a buffer | Aim 10 to 20 percent above the minimum to avoid extra consular scrutiny. |

| UK account planning | ISAs cannot receive new contributions post-move; plan your financial structure before applying. |

What I've learned from watching UK applicants get this wrong

After working with UK nationals on Spain residency applications, the pattern that stands out most is not underfunding. It is under-preparation. Applicants who have more than enough money still face delays because their documents tell a confusing story.

The biggest mistake I see is treating the financial package as an afterthought. Someone spends months researching neighborhoods in Valencia or Seville, then scrambles to pull together bank statements in the final two weeks before their consulate appointment. Apostilles take time. Certified translations take time. And if your statements show a large deposit that appeared last month, you have already undermined your own application.

My honest view is that UK applicants have a genuine advantage in this process because UK financial institutions produce clean, detailed statements that translate well for Spanish consulates. A Barclays or HSBC statement with 12 months of consistent balances is exactly what a consular officer wants to see. The problem is that most applicants do not give themselves enough time to compile that evidence properly.

The financial buffer recommendation is not just bureaucratic caution. It reflects real consular behavior. Officers who see funds sitting at exactly €28,800 know the applicant calculated the minimum. Officers who see €35,000 or more see someone who is genuinely financially settled. That psychological difference matters in discretionary decisions.

If you are relying on pension income rather than savings, get your pension provider to issue a formal annual income letter, not just a statement. And if your income comes from multiple sources, the cover letter approach is not optional. It is the difference between a clear application and a confusing one.

— Epic-residency

How Epic-residency helps UK nationals meet Spain's financial requirements

Epic-residency specializes in Spain residency applications for UK nationals, with particular depth in the Non-Lucrative Visa financial eligibility process. The team reviews your savings, pension, and investment documents to confirm they meet current IPREM thresholds, identifies gaps before your consulate appointment, and prepares the full financial package including cover letters and document checklists. If you are applying as a couple or family, Epic-residency calculates the exact dependent requirements and structures your proof of funds accordingly. For UK nationals who want their application handled correctly the first time, a consultation with Epic-residency is the most direct path to a successful outcome.

FAQ

What savings amount do UK nationals need for a Spain residency visa?

Single UK applicants need to demonstrate €28,800 in annual funds for 2026, calculated as 400% of Spain's IPREM. Each dependent added to the application requires an additional €7,200 per year.

Can UK savings accounts be used as proof of funds for the Spain NLV?

Yes. UK savings account balances from institutions like Barclays, HSBC, or NatWest are accepted, provided statements are apostilled and accompanied by a certified Spanish translation.

Does moving to Spain affect my UK ISA?

Existing UK ISAs remain open and continue to grow tax-free after you become non-resident, but you cannot make new contributions. The existing balance can be used as financial evidence for your Spain visa application.

What happens if my savings are only just above the minimum threshold?

Consulates may request additional documentation if your funds are marginally above the minimum IPREM multiple. Aim for at least 10 to 20 percent above the threshold to reduce the risk of extra scrutiny.

Can I work remotely while on a Spain Non-Lucrative Visa?

No. The NLV prohibits all forms of work in Spain, including remote work for foreign employers. Applicants planning to work while living in Spain should consider the Digital Nomad Visa instead.