UK pension Spain residency qualification is the process of meeting Spanish tax residency criteria so that the UK-Spain double taxation treaty governs where your pension income is taxed. Once you cross Spain's residency threshold, most UK pensions shift from HMRC's jurisdiction to Spain's Agencia Tributaria. The 2013 UK-Spain Double Taxation Convention, updated through the Multilateral Instrument, is the legal framework that determines every outcome. Understanding it before you move is not optional. It is the difference between a clean tax position and an expensive correction.

What are the Spanish tax residency criteria that affect UK pension access?

Spanish tax residency is the trigger that activates the UK-Spain treaty and reassigns your pension taxation rights. Spain uses two primary tests to determine whether you qualify as a tax resident in any given calendar year.

The first and most common test is physical presence. Spain considers you tax resident if you spend more than 183 days in the country within a single calendar year. Days are counted across the full calendar year, not a rolling 12-month period. This matters because arriving in Spain in July and staying through December can still push you past the threshold within that same tax year.

The second test is the center of vital economic interests. If Spain is where the core of your financial activity, investments, or business operations are based, you can qualify as a tax resident even without hitting 183 days. There is also a third, often overlooked trigger: if your spouse and dependent children reside in Spain, Spanish law presumes you are tax resident there unless you can prove otherwise.

The distinction between legal residence and tax residence trips up many UK retirees. Holding a Non-Lucrative Visa (NLV) or completing your empadronamiento (local registration) establishes legal residence. Tax residency is determined separately by actual presence and economic ties. You can be legally resident without being tax resident in year one, but that window closes quickly.

- Spending more than 183 days in Spain in any calendar year triggers tax residency automatically

- Having your primary economic base in Spain qualifies you even below 183 days

- A spouse and dependents living in Spain creates a legal presumption of your tax residency

- Legal residence (visa, registration) and tax residency are assessed under different rules

- Tax residency is assessed on a calendar year basis, meaning the year you move can count in full

Pro Tip: Keep a dated travel log from the day you arrive in Spain. A simple spreadsheet tracking entry and exit dates protects you if the Agencia Tributaria ever questions your residency year.

How does the UK-Spain double taxation treaty define pension taxation?

The 2013 UK-Spain Double Taxation Convention is the governing document for every UK pension you receive while living in Spain. Its rules are not suggestions. They are binding treaty obligations that override domestic tax law in both countries.

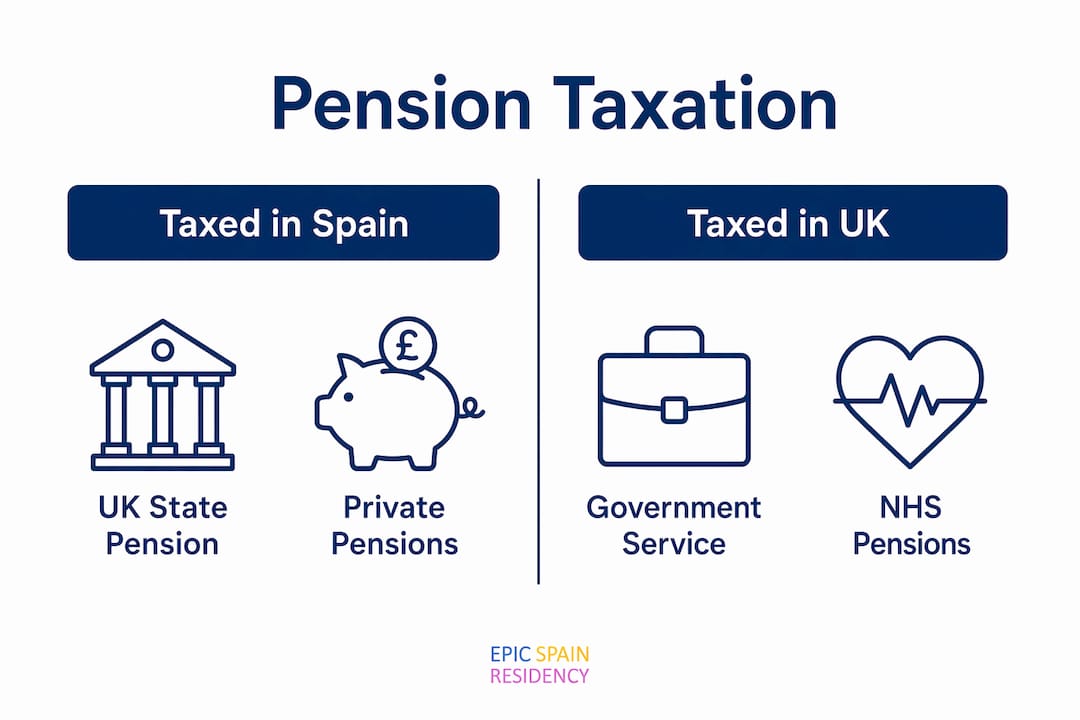

Under Article 17(1), pensions paid to a resident of one contracting state are taxable only in that state. Once you are a Spanish tax resident, this means Spain taxes your private pensions, SIPPs, and occupational pensions. The UK loses its right to tax that income. HMRC issues an NT (No Tax) code to your pension provider, stopping UK withholding at source.

There is one major exception that catches many retirees off guard. UK government service pensions remain taxable only in the UK, regardless of where you live. This covers NHS pensions, civil service pensions, teachers' pensions, and armed forces pensions. Spain cannot tax these. The UK retains exclusive taxing rights under the treaty carve-out. If you receive both a government service pension and a private pension, you face two separate tax regimes simultaneously.

| Pension type | Taxed in Spain as resident | Taxed in UK as resident |

|---|---|---|

| UK State Pension | Yes, under Article 18 | No |

| Private pension (SIPP, occupational) | Yes, under Article 17(1) | No |

| Government service pension (NHS, civil service) | No | Yes, exclusively |

| Mixed income (government + private) | Partially | Partially |

The UK State Pension sits under Article 18 rather than Article 17. Spanish tax residents receive it gross once HMRC issues form FD1, and Spain taxes it at savings-rate brackets. Spain's savings tax rates in 2026 run from 19% on the first €6,000 to 28% on income above €300,000. For most retirees, the effective rate on State Pension income sits between 19% and 21%.

Pro Tip: Request your HMRC NT code and FD1 form before your first pension payment as a Spanish resident. Retroactively reclaiming UK tax already withheld is possible but slow, often taking 12 to 18 months.

What practical steps are required to qualify as a Spanish resident for pension purposes?

Establishing qualifying residency for pension purposes involves both legal registration and tax administration steps. Neither alone is sufficient. You need both tracks running in parallel.

Legal registration steps:

- Apply for a Non-Lucrative Visa through the Spanish consulate in the UK before relocating. This is the standard route for UK retirees without employment income in Spain.

- Complete your empadronamiento at your local town hall (ayuntamiento) within 30 days of arrival. This registers you as a local resident and is required for most public services.

- Obtain your NIE (Número de Identificación de Extranjero), Spain's foreigner identification number. Every financial and tax transaction in Spain requires it.

- Apply for your TIE (Tarjeta de Identidad de Extranjero), the physical residence card issued after your visa is approved and you are in Spain.

Tax administration steps:

- Apply for a Spanish tax residency certificate from the Agencia Tributaria once you meet the residency criteria. This certificate is the essential document your UK pension providers and HMRC need to process treaty relief.

- Submit the certificate to HMRC alongside the relevant treaty relief application forms to trigger your NT code and, where applicable, form FD1 for State Pension.

- Notify each UK pension provider of your new tax status and provide the NT code reference.

- File an annual Spanish income tax return (Modelo 100) declaring all worldwide pension income, including government service pensions that remain UK-taxed.

Pro Tip: File your Modelo 100 even if you believe all your income is exempt in Spain. Declaring UK-taxed government service pensions on your Spanish return, while claiming the treaty exemption, creates a documented compliance record that protects you from future audits.

How do different UK pension types affect residency qualification and taxation outcomes?

Pension taxation depends primarily on residency status rather than the pension's origin, with one critical exception for government service pensions. Understanding which category your pension falls into determines your entire tax planning strategy.

- Private pensions (SIPPs, workplace pensions, occupational schemes): Fully taxable in Spain once you establish tax residency. HMRC stops UK withholding via the NT code. Spain taxes these as savings income.

- UK State Pension: Taxable in Spain under Article 18. Paid gross after FD1 form is issued. Spain taxes it at savings-rate brackets alongside your other pension income.

- Government service pensions (NHS, civil service, armed forces, teachers): Taxable only in the UK under the treaty carve-out. Spain cannot tax these, but you must still declare them on your Spanish return and claim the exemption.

- The 25% tax-free lump sum: This is one of the most damaging surprises for UK retirees. Spain does not recognize the UK's 25% pension commencement lump sum as tax-free. If you draw it after becoming a Spanish tax resident, Spain taxes the full amount as income. Drawing it before establishing Spanish residency is a legitimate and widely used planning strategy.

- Mixed pension income: Receiving both a government service pension and a private pension means managing two separate tax code arrangements and two reporting obligations. This dual treatment requires careful coordination between HMRC, the Agencia Tributaria, and each pension provider.

What are the key tax planning challenges when qualifying for UK pensions in Spain?

The year you move to Spain is the highest-risk period for pension taxation errors. Spanish tax residency can start in the calendar year of your move, meaning pension income received from January 1 of that year may fall under Spanish tax rules even if you only arrived in July.

Crossing the 183-day threshold is the most common trigger for UK retirees becoming Spanish tax residents, and it activates Spanish taxation of worldwide income retroactively for that calendar year. This is not a future liability. It applies to every pension payment you received in that tax year.

Key planning considerations include:

- ISA assets: UK ISA tax advantages do not transfer to Spain. Once you are a Spanish tax resident, ISA income and gains are taxable in Spain. Realizing ISA gains before establishing residency is a standard pre-move strategy.

- Pension lump sum timing: Draw your 25% tax-free lump sum before becoming a Spanish tax resident. After residency is established, Spain taxes the full withdrawal.

- Double taxation risk: Failing to apply for treaty relief on UK pensions can result in both HMRC and the Agencia Tributaria taxing the same income. The treaty prevents this, but only if you actively claim the relief.

- QROPS transfers: Qualifying Recognized Overseas Pension Scheme transfers to a Spanish-based scheme were once popular but carry a 25% overseas transfer charge in most post-Brexit scenarios. This option requires specialist advice before any action.

- S1 healthcare form: UK State Pension recipients can apply for an S1 form from HMRC, which entitles them to Spanish public healthcare funded by the UK. This is separate from tax residency but linked to your pension entitlement status.

"Pre-move pension crystallization and ISA gain realization are key strategies to optimize Spanish tax impacts upon residency transition." Source

Pro Tip: Book a cross-border tax consultation with a specialist who holds qualifications in both UK and Spanish tax law at least six months before your planned move date. The planning window closes the moment you cross the 183-day line.

Key takeaways

UK pension Spain residency qualification is governed by the 183-day rule, the UK-Spain Double Taxation Convention, and the specific pension type you hold, making early planning the single most important factor in your tax outcome.

| Point | Details |

|---|---|

| 183-day rule triggers residency | Spending more than 183 days in Spain in a calendar year makes you a Spanish tax resident. |

| Treaty governs pension taxation | Article 17(1) of the UK-Spain DTA assigns most pension taxation rights to Spain once you are resident. |

| Government pensions stay UK-taxed | NHS, civil service, and armed forces pensions remain taxable only in the UK under the treaty carve-out. |

| Draw lump sum before moving | Spain taxes the full pension lump sum; the UK's 25% tax-free allowance is not recognized in Spain. |

| Treaty relief must be claimed | Double taxation is only avoided if you actively apply for HMRC NT codes and Spanish residency certificates. |

What I've learned advising UK retirees on Spanish residency

The single biggest mistake I see UK retirees make is treating legal residence and tax residency as the same thing. They are not. You can hold a Non-Lucrative Visa, register at the town hall, and still not be a Spanish tax resident in year one if you manage your days carefully. That distinction is worth real money in some cases.

The second most common error is assuming the treaty works automatically. It does not. You have to file the paperwork, request the NT code, submit the FD1 form, and apply for the Spanish tax residency certificate. The treaty is a framework, not an automatic protection. Retirees who skip these steps often end up paying tax in both countries and spending years recovering overpaid UK tax through HMRC's repayment process.

For anyone with a government service pension alongside a private pension, the complexity doubles. You need separate tax arrangements for each income stream, and your Spanish tax return must reflect both correctly. I always recommend working with a gestor (Spanish tax advisor) who has specific experience with UK expat pension cases, not just general Spanish tax knowledge.

The 183-day rule for tax residency is not just a threshold to cross. It is a planning tool. Arriving in Spain after July 2 in any year means you cannot hit 183 days before December 31, giving you a full year to organize your tax affairs before Spanish residency kicks in. That is a strategy, not a loophole.

— Living

How Epic-residency helps UK retirees establish qualifying residency

Epic-residency specializes in helping UK nationals qualify for Spanish residency through the Non-Lucrative Visa, the most direct route for retirees living on pension income. The team handles the full application process, from income verification and document preparation to consulate submission and post-arrival registration. For UK pensioners, getting the Non-Lucrative Visa application right from the start avoids delays that can push your residency start date into the wrong tax year. Epic-residency also coordinates with clients' tax advisors to align visa timelines with pension planning strategies, so your legal residency and tax position work together rather than against each other. If you are planning a move to Spain in 2026, the time to start is now.

FAQ

Does the UK State Pension get taxed in Spain?

Yes. The UK State Pension is taxable only in Spain once you are a Spanish tax resident, under Article 18 of the UK-Spain Double Taxation Convention. HMRC issues form FD1 so it is paid gross, and Spain taxes it at savings-rate brackets.

How many days can I spend in Spain before becoming a tax resident?

You become a Spanish tax resident if you spend more than 183 days in Spain in a single calendar year. Staying 183 days or fewer keeps you below the threshold, though the center of economic interests test can still apply.

Are NHS and civil service pensions taxed in Spain?

No. Government service pensions, including NHS, civil service, teachers', and armed forces pensions, remain taxable only in the UK under the treaty carve-out in the UK-Spain Double Taxation Convention, regardless of where you live.

Can I take my 25% tax-free pension lump sum after moving to Spain?

Spain does not recognize the UK's 25% pension commencement lump sum as tax-free. Drawing it after establishing Spanish tax residency means Spain taxes the full amount. Drawing it before your residency start date avoids this outcome.

What visa do UK retirees need to qualify for Spanish residency?

The Non-Lucrative Visa is the standard route for UK retirees relocating to Spain. It requires proof of sufficient passive income, including pension income, to support yourself without working in Spain.